Learn Everything Concerning Residence Mortgages In This Short Article

Content author-Balslev Knudsen

A mortgage is truly a huge milestone in a person's life, whether they are 18 or 80 when they get it. The fact is that knowing the right things before you get started can make the process better. This article has what you need to know, so read it in full.

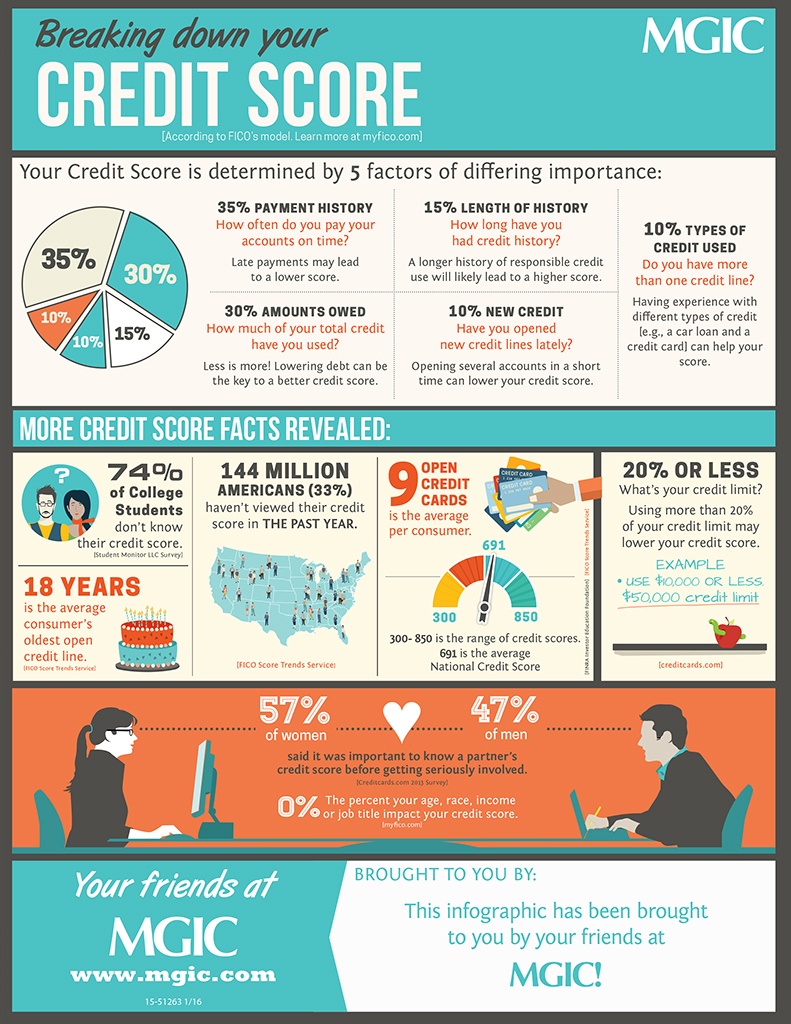

Understand your credit score and how that affects your chances for a mortgage loan. Most lenders require a certain credit level, and if you fall below, you are going to have a tougher time getting a mortgage loan with reasonable rates. A good idea is for you to try to improve your credit before you apply for mortgage loan.

When you're in the process of getting a home loan, pay off your debts and avoid new ones. When you apply for a home loan, lenders will look at how much debt you're carrying. If you have very little, you could be given a better loan for more money. A high level of debt can lead to your mortgage application being denied. Carrying debt may also cost you a lot of money by increasing your mortgage rate.

Get a pre-approval letter for your mortgage loan. A pre-approved mortgage loan normally makes the entire process move along more smoothly. It also helps because you know how much you can afford to spend. Your pre-approval letter will also include the interest rate you will be paying so you will have a good idea what your monthly payment will be before you make an offer.

Before getting a mortgage, study your credit history. Good credit is what can help you get a mortgage. Obtain copies of your credit history and scores from the three major credit-reporting bureaus. Study https://www.bloomberg.com/news/articles/2022-02-17/ubs-ceo-hamers-plays-down-bankers-titles-to-soften-hierarchy to ensure that no issues or errors must be resolved before you apply. Many lenders need a minimum score of 680, which complies with Freddie Mac and Fannie Mae's guidelines. Most lenders want to avoid scores that are lower than 620.

Watch out for banks offering a "no cost" mortgage loan. There is really no such thing as "no cost". The closing costs with "no cost" mortgages is rolled into the mortgage loan instead of being due upfront. This means that you will be paying interest on the closing costs.

Do not sign a home mortgage contract before you have determined that there is no doubt that you will be able to afford the payments. Just because the bank approves you for a loan does not mean that you could really endure it financially. First do the math so that you know that you will be able to keep the home that you buy.

Check out the interest rates for 15, 20 and 30 year term lengths. Many times the shorter the term length the lower the interest rate. Although you may think you payment will be higher on a shorter term loan, you can actually save money on your payment by choosing a lower interest rate and a shorter term.

Pay down your debt. You should minimize all other debts when you are pursuing financing on a home. Keep your credit in check, and pay off any credit cards you carry. This will help you to obtain financing more easily. The less debt you have, the more you will have to pay toward your mortgage.

Usually a mortgage that has a balloon rate is simple to get. This is a shorter term loan, and one that requires it to be refinanced after the expiration of the loan term. A balloon loan is risky since rates can increase by the time you need to refinance the balance you still owe.

Keep in visit my web page that not all mortgage lending companies have the same rules for approving mortgages and don't be discouraged if you are turned down by the first one you try. Ask for an explanation of why you were denied the mortgage and fix the problem if you can. It may also be that you just need to find a different mortgage company.

Do not pay off all of your old bills until you have talked to a mortgage consultant. If your bills will not have a negative impact on your ability to get a loan, you can worry about paying them later. You don't want to spend lots of money to pay them since this can affect the amount of available income you have.

Give yourself time to get ready for a mortgage. Even in an age of supposed instant Internet approvals, you need to take time preparing for a mortgage. This is time to clear your credit report, save money and maximize your score as much as possible. Give yourself at least six months in advance, although a year is better.

Be honest when it comes to reporting your financials to a potential lender. Chances are the truth will come out during their vetting process anyway, so it's not worth wasting the time. And if your mortgage does go through anyway, you'll be stuck with a home you really can't afford. It's a lose/lose either way.

Shop around for a mortgage broker that is a good fit for you. Remember that you are about to embark on a decades-long relationship with this lender, so you want to feel entirely comfortable dealing with the company. Do some online research, read reviews, look for lenders with excellent BBB ratings. Once you have sorted out a few, call and/or visit their offices. Apply with them and see if you can get a letter of pre-approval from the lender you eventually settle on.

Most financial institutions require that the property taxes and insurance payments be escrowed. This means the extra amount is added onto your monthly mortgage payment and the payments are made by the institution when they are due. This is convenient, but you also give up any interest you could have collected on the money during the year.

Compare different brokers when looking for a home mortgage. You need a good rate, of course. Also, take note of the wide variety of loans available to you. You should also add to your consideration the costs of closing and various other fees that are associated with buying a home.

You might have to investigate alternative sources as a means of getting a mortgage approval if your credit is bad, thin or nonexistent. Maintain records of all payments made for at least a year after making them. Borrowers that don't have a lot of credit can look better when they prove they have paid rent and utilities on time for a long while.

Now that you know what it takes to get a mortgage which fits your needs, you have to get down to work and do it. Follow the steps laid out here and begin your planning process. Soon enough, you'll find a great lender who is offering a great rate and your job will be done.